May update – FTSE hits records highs during the month as oil surges through $80

In May, The IFSL RC Brown UK Primary Opportunities Fund returned 2.75% compared with 2.82% for the FTSE All Share.

An extremely busy month for primary opportunities saw us participate in a number of attractive opportunities. We participated in placings in Zotefoams, Dairy Crest and Capita along with secondary placings in Charter Court Financial Services, Blue Prism and Sabre Insurance. We were active in the IPO market adding Urban Exposure, Rosenblatt and Avast to the portfolio.

The UK market continued its trend higher following a very strong April. Dollar strength and strong oil prices assisted the FTSE in hitting record highs. Even uncertainty over US tensions with Iran and the confirmation of trade tariffs being imposed on steel and aluminium imports into the US failed to shake the markets. Some retaliation is inevitable though this has failed to deter investor enthusiasm. Markets came off highs as a result of turmoil in Italy on concerns a further election would lead to a coalition of populist parties potentially putting Italy’s membership of the EU at risk.

Global M&A activity remained a feature with the first 4 months of the year being the highest on record. (Source: Dealogic) The UK market remains unloved offering relative value and its constituents subject to opportunistic bids from overseas buyers. This month saw Virgin Money bid for by CYBG, owner of Clydesdale Bank and Yorkshire Bank.

Purchases

Zotefoams

A company best know as a producer of foam materials for a wide range of industries including automotive, aerospace, construction and military. We acquired the shares as part of a £20m placing to fund a new manufacturing site in central Europe.

Dairy Crest

The UK’s largest cheese producer best known for its Cathedral City and Davidstow brands. We acquired the shares at a 6% discount to the previous night’s closing price as part of a £70m placing to increase its Davidstow plant capacity by 40%.

Capita

Capita has a had a torrid few years including ejection from the FTSE 100. The outsourcer which includes a broad range of financial and central government contracts raised £700m via a rights issue to reduce its debt and allow further investment. We acquired the shares as part of a rump placing – i.e. those shares not taken up by existing shareholders.

Charter Court Financial Services

We added to our holding in this challenger bank, having first purchased at IPO. We acquired the shares at a 6% discount to the previous night’s closing price following a sell down by private equity.

Blue Prism

Blue Prism is an artificial intelligence software company and considered to be one of the most exciting growth stocks on the UK market. We increased our holding following a management sell down of stock following the release of a strong trading statement.

Sabre Insurance

A car insurer with a market leading return on investment. We increased our holding, first purchased at IPO following a sell down by private equity.

Urban Exposure

A lender to small and medium sized house developers who have found it increasingly difficult since the financial crisis to borrow from the major banks. Enjoying high levels of return on equity, we took the opportunity to acquire the shares at IPO which will allow the Company to materially expand its lending book and improve return on equity further.

Rosenblatt

A London based law firm offering a comprehensive range of legal services with particular strength in the property and litigation sectors. We acquired the shares at IPO where funds were raised to further modernise the Company and for anticipated acquisitions. The shares have enjoyed an impressive start to listed life, rising over 30%.

Avast

Avast is a provider of security software to the consumer, a challenger to the likes of Norton and McAfee. Seen as a disruptor in the industry by offering a basic product for free, in the belief customers will upgrade to a more comprehensive subscription product. It is the largest IPO in London in 2018 to date with a market capitilisation in excess of £2bn.

Sales

Royal Dutch Shell

We modestly reduced the Fund’s largest holding following a rising share price boosted by recent strong oil prices. The shares have more than doubled from their lows in early 2016. With a dividend yield over 5% it remains an attractive long term holding.

Diversified Oil & Gas

We took profits on our modest holding following strength in the oil price that had boosted the whole sector. We do not have strong views on the future oil price but given its recent sharp increase on geopolitical uncertainty, we believe that in the short term, it will pause for breath, thus limiting the upside for the sector.

Fulcrum Utility Services

We sold our remaining holding for a solid profit in order to fund upcoming primary opportunities.

Unite Group

We sold our remaining holding for a solid profit following strong recent performance and to fund upcoming primary opportunities.

Treatt

The holding was reduced on strength following a good market update. With stock markets at fresh highs we felt it an opportune time to reduce our holdings in some of our more highly rated stocks.

Primary Health Properties

Strong share price performance following its recent share placing and its inclusion in the FTSE 250 (resulting in index buyers) led us to reduce our holding with the Company again trading at a premium to NAV.

Legal & General

We had purchased our holding in a rare secondary market foray during the sharp global sell off in stock markets earlier in the year. As anticipated, this turned out to be a setback rather than anything worse and with markets recovering and hitting new highs, we took the opportunity to crystallise our double digit gains.

Galliford Try

We reduced our holding following a solid trading update that was well received by the market.

Premier Asset Management

We reduced our holding following a good results’ statement that was well received by the market. The Company has also been aided by record stock market levels, hence we felt it prudent to take some profits in a Company that has doubled in the 18 months since we purchased at IPO.

Hollywood Bowl

We reduced our holding following a strong set of results that were well received by the market. Following the recent placing in Ten Entertainment Group which is now one of our largest holdings, we considered it prudent to reduce our exposure to ten pin bowling elsewhere in the portfolio.

Fever-Tree

The undoubted star of our portfolio. We took the opportunity to reduce our holding as the stock hit fresh highs of over £30, having first purchased at IPO in 2014 at £1.34. Whilst we remain excited by the potential of the brand in the US, we are mindful of the stock’s very high rating which leaves little room for disappointment.

Easyhotel

Having performed very strongly since its recent share placing, we took some profits following a well received market update.

Sirius Real Estate

Having purchased the shares at a discount to NAV, recent strength has seen them recover to now trade at a premium, allowing us to sell for a double digit gain.

JTC

We reduced our holding following the recent successful IPO and the Company’s inclusion in the FTSE All Share which has led to a share price squeeze. The shares have gained more than 30% since IPO in March.

Cumulative Performance (Total Return %)– May 2018

| Fund/Benchmark Name | Year to 30/05/2018 | 3 Years to 30/05/2018 | 5 years to 30/05/2018 |

|---|---|---|---|

| IFSL RC Brown UK Primary Opportunities P Acc | 6.04 | 36.52 | 62.41 |

| IA UK All Companies | 6.62 | 23.11 | 50.40 |

| FTSE All Share | 6.15 | 24.64 | 45.40 |

Discrete Annual Performance (Total Return %) – May 2018

| Fund/Benchmark Name | 30/05/2017 to 30/05/2018 | 30/05/2016 to 30/05/2017 | 30/05/2015 to 30/05/2016 | 30/05/2014 to 30/05/2015 | 30/05/2013 to 30/05/2014 |

|---|---|---|---|---|---|

| IFSL RC Brown UK Primary Opportunities P Acc | 6.04 | 28.00 | -0.27 | 8.33 | 10.53 |

| IA UK All Companies | 6.62 | 21.59 | -5.72 | 10.32 | 11.52 |

| FTSE All Share | 6.15 | 24.52 | -6.31 | 7.47 | 8.86 |

Source: FE 2018

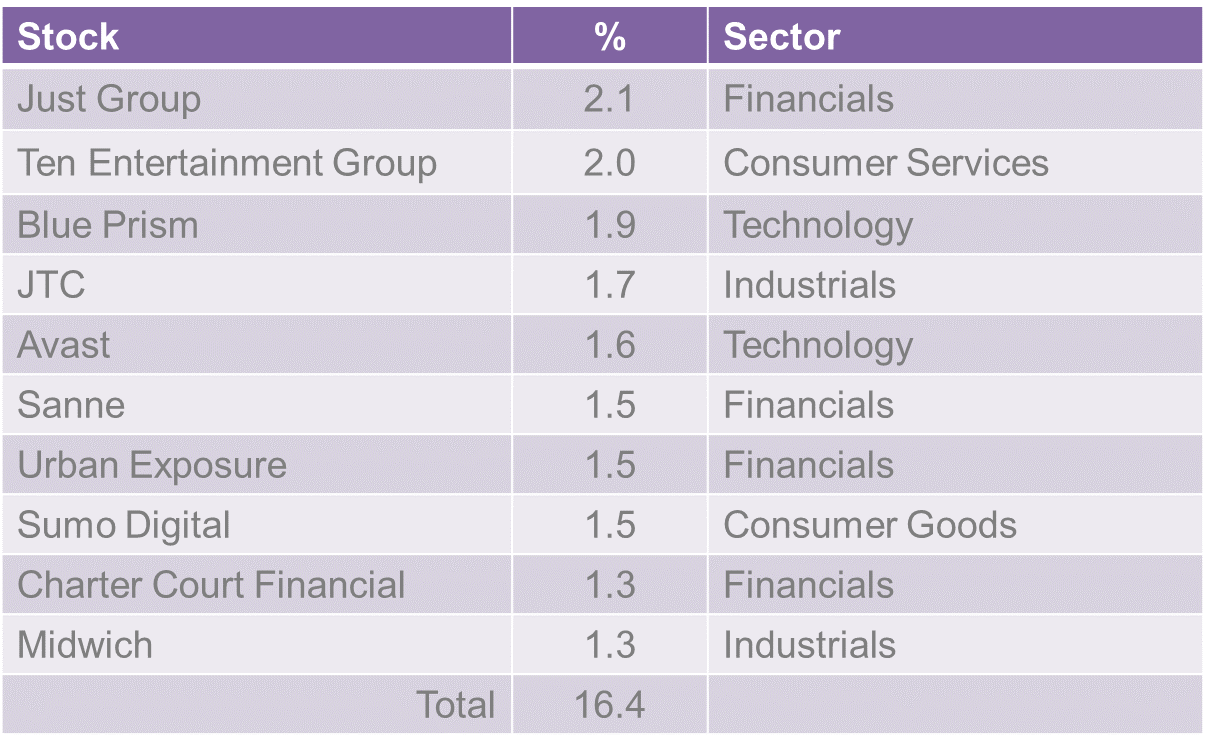

Top Ten Active Holdings

Source: RCBIM as at 31 May 2018

The past is not necessarily a guide to future performance. Investments and the income derived from them can fall as well as rise and the investor may not get back the amount originally invested. R.C. Brown and Marlborough are authorised and regulated by the FCA. Marlborough are the ACD. The Key Investor Information Document and the Full Prospectus can be obtained via www.marlboroughfunds.com or by request at: info@rcbpo.co.uk