January update – 2019 starts with a market snap back following a difficult year for equities in 2018

We participated in one primary opportunity in January – Savannah Petroleum. Unsurprisingly a quiet month for corporate activity after the Christmas lay off, we are aware of a growing pipeline of potential future primary opportunities which we shall appraise and consider for investment. We turned down two opportunities in January which did not meet our investment criteria.

In January, the IFSL RC Brown UK Primary Opportunities Fund returned +3.65% compared with +4.18% for the FTSE All Share and +5.42% for the IA UK All Companies Sector. (Please be advised that the past is not necessarily a guide to future performance. Investments and the income derived from them can fall as well as rise and the investor may not get back the amount originally invested) We gave up some of our recent outperformance – the main reasons being our lower exposure to mid cap companies, and in particular UK domestic names. It has been a long while since we have held housebuilders and larger retailers. January saw a strong recovery in these names following market updates that were no worse than feared. Whilst we have added to our UK domestic exposure in recent months with the purchases of Kier and Grainger, we remain cautious over the political environment and await a more certain outlook. Our cash position has risen to 10% giving us firepower for forthcoming primary opportunities and to take advantage of further market volatility.

Markets recovered their poise following a rotten end to 2018. The main reason for the recovery was a more dovish narrative emanating from the Federal Reserve – meaning expectations of future interest rate rises will be more moderate as the global economic growth slows. There is also renewed hope that China and the US will come to a trade agreement, brought into focus by Apple’s sales warning citing the trade war as a headwind.

We continue to consider the UK market to be unloved and offering value. With a UK market dividend yield in excess of 4%, regardless of the inevitable volatility, we are paid to wait and we believe greater certainty over Brexit and the health of the global economy will emerge in coming months.

Purchases

Savannah Petroleum

Savannah is an oil and gas Company with assets in Niger and is close to completing the purchase of assets in Nigeria. We participated in a placing at a 9% discount to the previous night’s closing price as the Company raised $23m for working capital purposes. We believe the assets in Nigeria offer compelling value alongside the hope of further finds in Niger. The Company is shortly to commence dividend payments – a rarity amongst smaller oil and gas companies.

Sales

Premier Asset Management

The smallest holding in our portfolio was sold following a strong update, despite difficult market conditions for fund managers. We used the share price rise to take profits.

International Public Partnerships

We halved our holding in what had been our largest active position following a period of outperformance. This infrastructure stock has held up well in the market turmoil and we took the opportunity to take profits.

Kier

We trimmed our holding following what we considered to be a bear squeeze as, following a satisfactory market update, hedge funds found themselves short of stock, resulting in a share price spike. Having gained more than 20% in a matter of weeks, we used this an opportunity to take some profits.

Urban Exposure

A disappointing performer since IPO in 2018, we took advantage of liquidity to exit our holding in this lender to smaller housebuilders. We had become concerned about a changing strategy to that set out at IPO and hence felt our capital better deployed elsewhere.

Sanne

One of strongest performer since purchase at IPO in 2014, following the surprise departure of the CEO and a tepid market update, we decided to sell our remaining holding in this business outsourcing Company.

Arena Events

A concerning market update, citing rising costs, led us to sell our holding in this supplier of temporary seating and structures to a range of blue chip sporting events.

Cumulative Performance (Total Return %)– January 2019

| Fund/Benchmark Name | Year to 31/01/2019 | 3 Years to 31/01/2019 |

5 years to 31/01/2019 |

Since Inception (28/05/1997) |

|---|---|---|---|---|

| IFSL RC Brown UK Primary Opportunities P Acc | -4.34 | 35.34 | 42.57 | 376.64 |

| Quartile Ranking – IA UK All Cos | 2 | 1 | 1 | 1 |

| IA UK All Companies | -5.62 | 24.80 | 27.86 | 240.91 |

| FTSE All Share | -3.83 | 28.49 | 31.24 | 258.72 |

Discrete Annual Performance (Total Return %)– January 2019

| Fund/Benchmark Name | 31/01/2018 to 31/01/2019 | 31/01/2017 to 31/01/2018 | 31/01/2016 to 31/01/2017 | 31/01/2015 to 31/01/2016 | 31/01/2014 to 31/01/2015 |

|---|---|---|---|---|---|

| IFSL RC Brown UK Primary Opportunities P Acc | -4.34 | 18.13 | 19.78 | 2.14 | 3.14 |

| Quartile Ranking – IA UK All Cos | 2 | 1 | 2 | 1 | 4 |

| IA UK All Companies | -5.62 | 12.45 | 17.60 | -3.30 | 5.94 |

| FTSE All Share | -3.83 | 11.28 | 20.06 | -4.63 | 7.11 |

Source: FE 2019

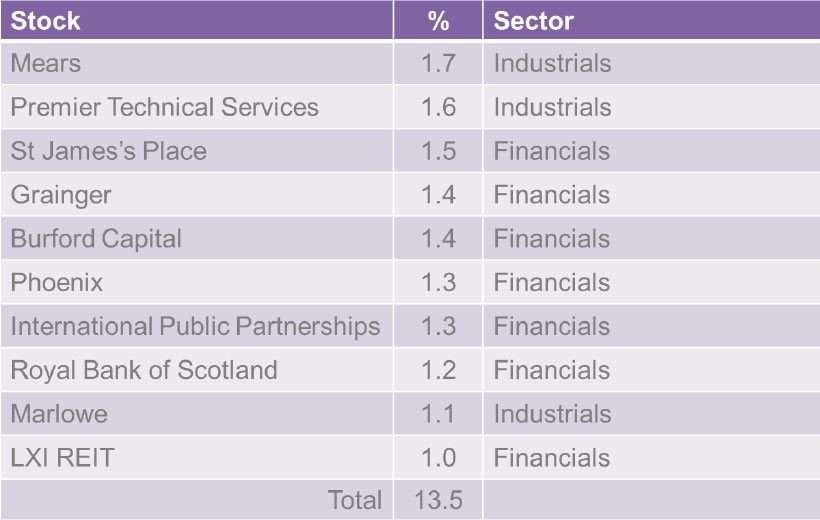

Top Ten Active Holdings

Source: RCBIM as at 31 January 2019

The past is not necessarily a guide to future performance. Investments and the income derived from them can fall as well as rise and the investor may not get back the amount originally invested. R.C. Brown and Marlborough are authorised and regulated by the FCA. Marlborough Fund Manager are the ACD. The Key Investor Information Document and the Full Prospectus can be obtained via www.marlboroughfunds.com or by request at: info@rcbpo.co.uk