March update – the IPO market opens for 2019 as the Fund invests in 2 IPO’s

We participated in four primary opportunities in March – DWF, Diaceutics, PPHE Hotel Group and Astrazeneca whilst also adding RELX to the portfolio at a time of weakness. We are seeing a growing pipeline of potential deals despite the political uncertainty. DWF became the largest IPO in the UK in 2019 to date. We often end up making our best investments in times of difficulty as shares need to be more keenly priced. As the Company then proves itself and buoyancy returns to markets, we would expect a material re-rating.

In March, the IFSL RC Brown UK Primary Opportunities returned +2.19% compared with +2.67% for the FTSE All Share and +1.82% for the IA UK All Companies Sector.

Markets made good progress during the month, albeit large caps markedly outperformed the more UK focused mid and small caps. Hopes of a softer Brexit saw the UK market hit highs for the year, whilst M&A remained a feature with mid cap satellite operator Inmarsat attracting a takeover bid. Towards month end saw increased volatility on fears of stalling US growth and a more dovish tone from the Federal Reserve.

Despite the ongoing political shenanigans, which of course have further to run, we continue to believe the UK market to be unloved and offering value. With a UK market dividend yield in excess of 4%, regardless of the inevitable volatility, we are paid to wait and we believe greater certainty over Brexit and the health of the global economy should emerge in coming months.

Please be advised that the past is not necessarily a guide to future performance. Investments and the income derived from them can fall as well as rise and the investor may not get back the amount originally invested

Purchases

DWF

DWF is a mid market, full service, UK focused law firm, albeit with operations in over a dozen countries. We purchased the shares at IPO with the proceeds to be used for investment in technology, new team hires and further overseas expansion. On a modest rating and a prospective dividend yield of over 5%, we considered it an attractive IPO in what are difficult markets for new companies. The shares are currently trading around their IPO price.

Diaceutics

Diaceutics is a data analytics business servicing the global pharmaceutical industry, aiding them to deliver precision medications, producing better patient outcomes. We purchased shares at IPO with the funds raised to be used to grow the business further. A profitable business in an exciting sector with a blue chip client base. The shares have already appreciated 30%.

PPHE Hotel Group

Park Plaza Hotels Europe has an estate of high quality hotels across Europe’s leading cities. Its largest exposure is the UK though is looking to further expand into Europe. It also owns the art’otel brand which has a more boutique feel. We acquired the shares as part of a placing of the major shareholders stake, who have reduced their holding to under 50%. We acquired the shares at an 8% discount to the previous night’s closing price. We anticipate the shares being admitted to the FTSE 250 which should drive further demand for the shares.

RELX

Formerly known as Reed Elsevier and a constituent of the FTSE 100. RELX publishes scientific, technical and medical material along with legal textbooks and operates and exhibitions. With 30,000 employees in 40 countries, it is a truly global business. We made a relatively rare purchase in the secondary market following its sharpest share price fall in a decade on the University of California’s decision to cancel its contract with the Company. We considered the share price fall over done and were content to add a relatively defensive, solid dividend paying stock to our portfolio.

Astrazeneca

One of the largest listed companies on the London market, raised £2.7bn to help fund the purchase of rights for a next generation cancer treatment, which further funds the growth profile of the Company. Already one of our largest holdings, we took advantage of the shares being placed at a 6% discount to the previous night’s closing price. The shares are a core holding and now the third largest holding in the Fund.

Sales

Blue Prism

With a near 40% gain inside a month, we trimmed our holding in this fast growing Artificial Intelligence Company.

XPS Pension Group

A pensions consultancy group which has not performed well since the merger between Xafinity (which we acquired at IPO) and Punter Southall. A small holding and we decided to cut our modest losses, taking advantage of liquidity.

Kier Group

With the shares of this construction and maintenance company proving extremely volatile, we took advantage of a price spike earlier in the month before selling the remainder of our holding on results, providing a near 20% gain on our investment this year.

TI Fluid Systems

With cyclical companies enjoying a surge so far this year, we trimmed our holding in this automotive fluid systems company on strength. The shares remain cheap, albeit highly geared to global economic conditions.

Sabre Insurance

A solid performer for the portfolio, particularly given market volatility over the past six months. We sold our holding, taking profits, following this month’s results statement.

Aston Martin Lagonda

Following an uninspiring update, we decided to cut our losses in what has not been a good investment. Whilst we accept the shares were fully priced at IPO, the sharp deterioration in risk sentiment since IPO and de-rating of growth stocks has been marked. We are content to sit on the sidelines for the time being in the knowledge there will be further primary opportunities in the Company and we can regain confidence that the Company will hit its 2021-22 production targets.

Cumulative Performance (Total Return %)– March 2019

| Fund/Benchmark Name | Year to 31/03/2019 | 3 Years to 31/03/2019 |

5 years to 31/03/2019 |

Since Inception (28/05/1997) |

|---|---|---|---|---|

| IFSL RC Brown UK Primary Opportunities P Acc | 5.56 | 40.63 | 44.45 | 387.09 |

| Quartile Ranking – IA UK All Cos | 2 | 1 | 1 | 1 |

| IA UK All Companies | 2.80 | 25.93 | 28.90 | 247.73 |

| FTSE All Share | 6.36 | 32.81 | 34.32 | 266.9 |

Discrete Annual Performance (Total Return %)– March 2019

| Fund/Benchmark Name | 31/03/2018 to 31/03/2019 | 31/03/2017 to 31/03/2018 | 31/03/2016 to 31/03/2017 | 31/03/2015 to 31/03/2016 | 31/03/2014 to 31/03/2015 |

|---|---|---|---|---|---|

| IFSL RC Brown UK Primary Opportunities P Acc | 5.56 | 5.60 | 24.98 | -0.21 | 3.31 |

| Quartile Ranking – IA UK All Cos | 2 | 1 | 1 | 2 | 4 |

| IA UK All Companies | 2.80 | 2.65 | 17.95 | -2.41 | 5.77 |

| FTSE All Share | 6.36 | 1.25 | 21.95 | -3.92 | 6.57 |

Source: FE 2019

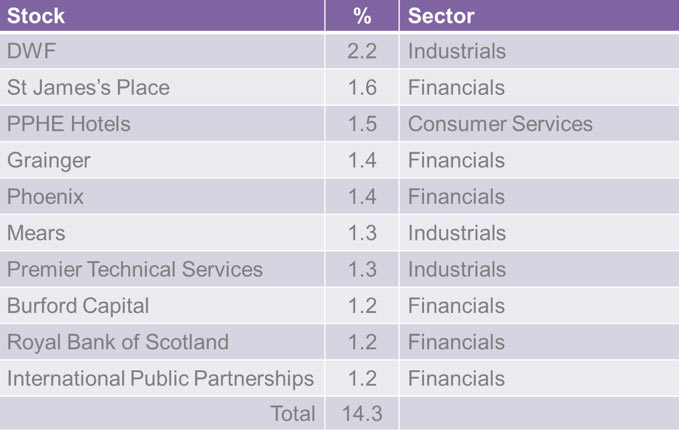

Top Ten Active Holdings*

Source: RCBIM as at 31 March 2019

*Active holding relates to the overweight position relative to the stock’s FTSE All Share weighting

The past is not necessarily a guide to future performance. Investments and the income derived from them can fall as well as rise and the investor may not get back the amount originally invested. R.C. Brown and Marlborough are authorised and regulated by the FCA. Marlborough Fund Manager are the ACD. The Key Investor Information Document and the Full Prospectus can be obtained via www.marlboroughfunds.com or by request at: info@rcbpo.co.uk